Wage Garnishment Explained: What It Is, How It Happens, and What It Means

By IRS Notices Explained Editorial Team | Reviewed for legal context by David McNickel

An IRS wage garnishment – officially called a wage levy – is when the IRS requires your employer to withhold money from your paycheck and send it directly to the IRS to pay your tax debt.

Many people feel alarmed when they learn their wages might be garnished, but understanding how this works can reduce anxiety. Wage garnishment doesn’t happen suddenly – it follows a specific legal process with notices and opportunities to respond. This article explains what wage garnishment is, how it develops, and what it typically means for your financial situation. For a broader explanation of how the IRS enforces tax debts, see our guide to IRS enforcement actions.

What a Wage Garnishment Is

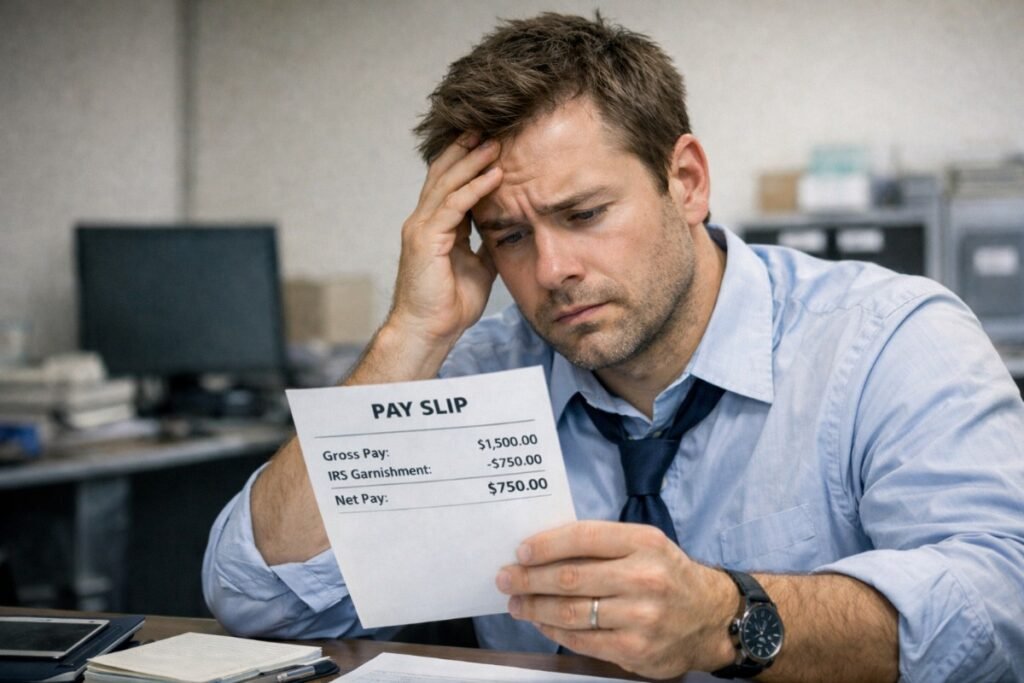

A wage garnishment is a legal order that directs your employer to withhold a portion of your earnings and send it to the IRS to satisfy unpaid tax debt. The IRS refers to this as a wage levy, and it’s one of the most common collection tools the agency uses. When your wages are garnished, the money is taken before you receive your paycheck, meaning you see less income in your bank account or on your pay stub.

The IRS calculates how much can be taken based on your filing status and number of dependents, leaving you with a minimum amount intended for basic living expenses. Unlike some other types of garnishment that take a percentage of your wages, IRS wage garnishments take most of your disposable income, leaving only the protected amount. This continues pay period after pay period until the tax debt is satisfied or the garnishment is released.

How the IRS Gets to This Point

Wage garnishment doesn’t occur without extensive prior communication. The process begins when you have an unpaid tax debt. The IRS first sends notices informing you of the balance and requesting payment. If these notices go unanswered or payment isn’t arranged, the IRS escalates its collection efforts.

Before garnishing your wages, the IRS must send you a Final Notice of Intent to Levy. This notice, sent at least 30 days before the levy begins, informs you of the IRS’s intent and gives you the right to a Collection Due Process hearing.

During this 30-day period, you have opportunities to pay the debt, set up a payment plan, or request the hearing. The IRS typically sends these notices to your last known address, so it’s important that your address on file is current. The timeline from initial notice to wage garnishment usually spans several months, involving multiple communication attempts from the IRS.

What Typically Triggers a Wage Garnishment

Several situations commonly lead to wage garnishment. The primary trigger is an unpaid tax balance that hasn’t been addressed despite IRS notices. When someone doesn’t respond to payment demands or doesn’t arrange an installment agreement, the IRS may move forward with garnishment. Breaking an existing payment plan can also trigger wage garnishment – if you had an arrangement but stopped making payments, the IRS may resort to this collection method.

Ignoring the Final Notice of Intent to Levy is particularly significant, as that notice represents your last opportunity to address the situation voluntarily before the garnishment begins. Some people receive notices but don’t understand what action is required. Others face financial hardship and can’t pay, but they don’t communicate with the IRS about their situation. The IRS generally pursues wage garnishment when it appears to be an effective way to collect the debt and other methods haven’t worked. Check here for information on Student Loan Wage Garnishment. For more on Wage Garnishmen in general, check this resource.

What This Enforcement Action Can Affect

Wage garnishment directly affects your take-home pay. When the garnishment is in place, you’ll see a significant reduction in the amount of money you receive each pay period. The IRS calculates the exempt amount – what you’re allowed to keep – based on your filing status and number of dependents.

For example, someone who is single with no dependents has less protected income than someone married with children. The remaining amount after this exemption is taken by the IRS. This can create immediate financial strain, making it difficult to pay rent, mortgages, utilities, or other regular expenses.

Your employer becomes involved in the process, as they’re legally required to comply with the garnishment order. They receive notice from the IRS and must begin withholding according to the instructions. While this shouldn’t affect your employment status – employers cannot terminate you simply because of a federal tax garnishment – it does mean your employer is aware of your tax situation.

The garnishment continues with each paycheck until the debt is fully paid or the IRS releases the levy. If you change jobs while a garnishment is in place, the IRS will typically issue a new garnishment order to your new employer once they become aware of the change.

Is This the Same for Everyone?

No. Wage garnishment situations differ significantly from person to person. The amount of your paycheck that’s protected from garnishment depends on your filing status and how many dependents you claim. Someone with a spouse and multiple children will have more income protected than someone who is single.

The total amount owed varies – some people have garnishments that last a few months, while others experience them for a year or longer depending on the debt size and their income level. People with higher incomes may pay off the debt more quickly, while those with lower incomes may find the garnishment lasts longer. Some individuals face garnishment on only one tax year’s debt, while others owe for multiple years.

The financial impact also varies based on your existing expenses and obligations – someone with high fixed costs like rent or mortgage may experience more hardship than someone with lower expenses.

How This Fits Into the IRS Collection Process

Wage garnishment is a mid-to-late-stage collection action. It typically occurs after the IRS has tried other methods to collect the debt. The usual progression looks like this:

- first, a tax debt is assessed;

- second, the IRS sends initial notices and payment demands;

- third, the IRS may file a Notice of Federal Tax Lien to establish its claim;

- fourth, more urgent notices are sent;

- fifth, a Final Notice of Intent to Levy is issued with Collection Due Process hearing rights;

- sixth, if no resolution is reached, the wage garnishment begins.

Wage garnishment represents a point where the IRS has moved from requesting payment to taking it directly from your income. If the garnishment alone doesn’t satisfy the entire debt, the IRS may also pursue other assets through additional levies. Understanding this progression shows that garnishment is a serious collection step that comes after multiple opportunities to address the debt voluntarily.

Common Questions About a Federal Tax Lien

Does this happen without notice?

No. Federal law requires that the IRS send you a Final Notice of Intent to Levy at least 30 days before garnishing your wages. You receive multiple opportunities to respond.

Can this be stopped or paused?

Wage garnishments can potentially be released if

- you pay the debt in full,

- set up an approved installment agreement,

- qualify for Currently Not Collectible status,

- demonstrate economic hardship.

Requesting a Collection Due Process hearing can also delay the start of garnishment.

Does this mean my situation is serious?

Yes. Wage garnishment indicates the IRS is taking direct action to collect after other attempts haven’t resolved the debt. It reflects escalation in the collection process.

How long does this usually last?

The garnishment continues until the tax debt is paid in full or the IRS releases the levy. This could be several months to over a year, depending on the amount owed and your income.

Does this affect my credit?

The garnishment itself doesn’t directly appear on credit reports, though the underlying tax debt and any associated lien may. If the garnishment causes you to miss other payments, that could impact your credit.

Can my employer fire me because of this?

Federal law prohibits employers from terminating an employee solely because of a federal tax garnishment. However, your employer will be aware of the garnishment.

How much of my paycheck can the IRS take?

The IRS takes most of your disposable income, leaving you with an exempt amount based on your filing status and dependents. This is often significantly more than other types of garnishment.

What Options People Typically Consider at This Stage

When facing wage garnishment, people evaluate several approaches. Some work to pay the balance in full if they can access funds, which results in immediate release of the garnishment. Others contact the IRS to establish an installment agreement, which may lead to garnishment release if approved. Some request a Collection Due Process hearing before the garnishment starts to present their case and explore alternatives.

Those experiencing financial hardship may apply for Currently Not Collectible status or request levy release based on inability to meet basic living expenses. Some people review their withholding and exemptions with the IRS to ensure the calculation is correct. Others examine whether they can adjust their budget to manage on the reduced income while the garnishment is in place. Each approach depends on individual financial circumstances and the specific amount owed.

When People Usually Seek Professional Help

Many people consider professional assistance when dealing with wage garnishment. Common situations include when they’ve received a Final Notice of Intent to Levy and want help understanding their options before the garnishment starts. People often seek help once garnishment has begun and they’re struggling to meet basic expenses.

Those with substantial tax debt who are uncertain about the best resolution path may consult with professionals. If someone wants to request a Collection Due Process hearing but doesn’t understand the procedures, professional guidance may be helpful.

People with multiple tax years of debt or complex financial situations sometimes find professional assistance valuable for navigating their options. Self-employed individuals or business owners facing garnishment may seek help understanding how it affects their specific circumstances. The decision to seek help is personal and relates to individual comfort with handling tax collection matters independently.

Key Takeaways

- Wage garnishment is a legal order requiring your employer to send a portion of your paycheck to the IRS for unpaid tax debt

- The process includes multiple notices, with a mandatory 30-day warning before garnishment begins

- The IRS takes most of your disposable income, leaving only an exempt amount based on filing status and dependents

- Wage garnishment is a mid-to-late-stage collection action that continues until the debt is resolved

- Options for addressing garnishment include payment arrangements, hardship release, or requesting a Collection Due Process hearing

What To Read Next

This page provides general informational content only and is not affiliated with the IRS or any government agency.