IRS Notice CP14 Explained: What It Means and What Happens Next

By IRS Notices Explained Editorial Team | Reviewed for legal context by David McNickel

If you’ve received IRS Notice CP14, you’re likely wondering what it means and whether you need to take immediate action. This notice is the IRS’s first formal letter informing you that you have an unpaid balance from a tax return you filed. It’s the initial step in the IRS collection process, sent when the agency’s records show you owe money.

While it does require attention, CP14 is not an emergency notice – it’s an informational letter that starts a timeline you should be aware of. The CP14 is one of several IRS balance due notices. You can review all notice types in our IRS Notices guide.

What IRS Notice CP14 Is

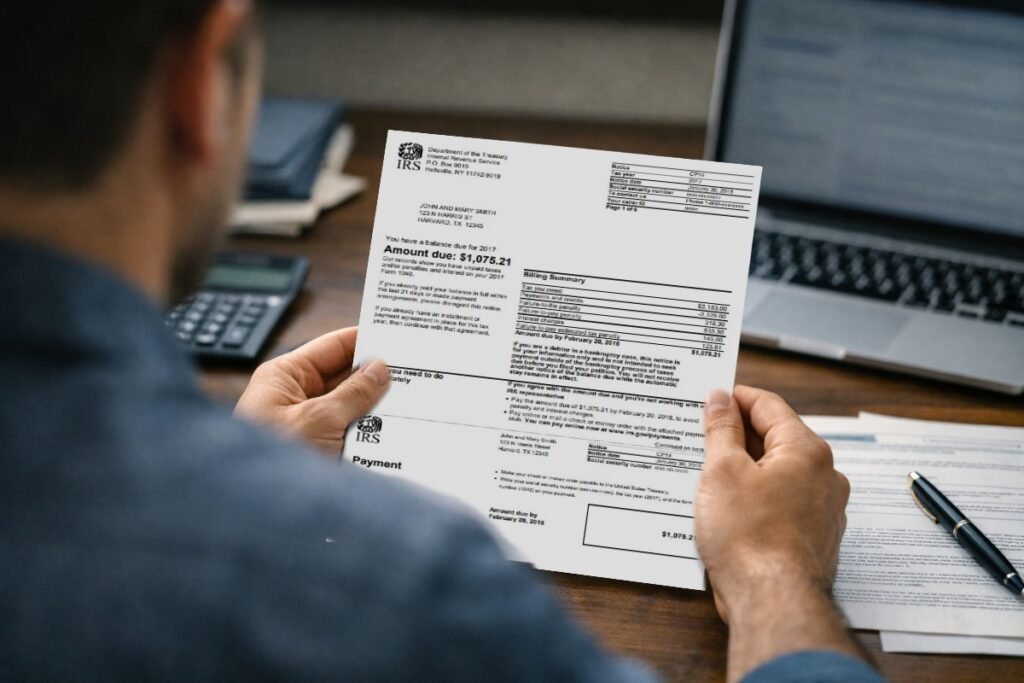

IRS Notice CP14 is the first notice the IRS sends when their records indicate you have an outstanding tax balance. This is typically sent after you’ve filed a tax return that showed a balance due, or after the IRS processed your return and determined you owe more than you paid. The notice will state the amount you owe, including the original tax debt plus any penalties and interest that have accrued. It serves as both a billing statement and a request for payment. While immediate payment is requested, this notice does not threaten enforcement actions like liens or levies. It’s essentially the IRS saying, “Our records show you owe this amount—please pay it or contact us.”

Why You Received This Notice

There are several common reasons why taxpayers receive a CP14 notice:

You filed a tax return that showed a balance due but didn’t include payment with your return. The IRS processed your return and is now billing you for the amount owed. You made a partial payment with your return, but it didn’t cover the full amount due. The IRS made adjustments to your return after processing it, resulting in additional tax owed. You had a payment plan from a previous year that was completed, but you now owe for a new tax year. You requested an extension to file but didn’t make an estimated payment, and your filed return showed a balance. The notice should clearly state which tax year and tax form the balance relates to, so you can verify the amount against your own records.

What the IRS Is Asking You to Do

The CP14 notice requests that you pay the full amount due by the date specified in the letter – typically 21 days from the notice date. The notice will include payment options such as paying online, by phone, by check, or through direct debit. If you cannot pay the full amount immediately, the notice may mention that payment plan options exist, though specific instructions might not be detailed in this first letter. The IRS expects you to either pay in full, make arrangements to pay, or contact them if you believe the amount is incorrect. While responding is strongly encouraged, this notice does not legally require a written response unless you’re disputing the amount owed.

What Happens If You Ignore This Notice

If you don’t respond to CP14 or make payment arrangements, the IRS collection process continues automatically. You’ll receive additional notices over the following weeks and months, each becoming progressively more serious in tone. The balance will continue to accrue penalties and interest – typically the failure-to-pay penalty is 0.5% of the unpaid amount per month, plus interest that compounds daily.

After CP14, you can expect to receive a CP501 notice (first reminder), followed by a CP503 (second reminder), and eventually CP504 (final notice before enforcement action). Ignoring these notices can ultimately lead to tax liens being filed against your property or levies against your bank accounts or wages. However, these enforcement actions don’t happen immediately after a single ignored notice – the process typically takes several months to a year.

How This Notice Fits Into the IRS Collection Timeline

CP14 is the first notice in the standard IRS collection sequence. It represents the beginning of the formal collection process, though it’s important to note that penalties and interest began accruing from the original due date of your tax return. Before CP14, you may have received a tax bill with your return or a balance due notice, but CP14 is the first official collection notice.

After CP14, if payment isn’t received, the typical sequence includes CP501 (sent about 5 weeks after CP14), CP503 (sent about 7 weeks after CP501), and CP504 (the final notice of intent to levy, sent several weeks after CP503). Understanding this timeline helps you see where you are in the process – CP14 gives you the most time and the most options before any enforcement actions are considered.

Common Questions About The IRS CP14 Notice

Is this notice serious?

It’s the first formal collection notice, so it should be taken seriously, but it’s not an emergency. You have time to respond and explore options.

Do I need to respond right away?

The IRS requests payment within 21 days, but responding within that timeframe—even to set up a payment plan—is advisable to prevent additional notices.

Can I pay later or set up payments?

Yes, the IRS offers payment plan options, though CP14 may not detail all of them. You can contact the IRS or apply for a payment plan online.

Does this mean enforcement is coming?

Not immediately. CP14 is the first notice. Enforcement actions like levies or liens only occur after multiple notices have been ignored, typically many months later.

Can penalties be reduced?

In some cases, penalties can be abated if you have reasonable cause or qualify for first-time penalty abatement, but interest generally cannot be removed.

What if I think the amount is wrong?

You should contact the IRS at the number on the notice to discuss the discrepancy. Bring documentation that supports your position.

Will this affect my credit score?

CP14 itself won’t affect your credit. However, if the debt remains unpaid and the IRS files a Notice of Federal Tax Lien, that could impact your credit.

What Options People Typically Consider at This Stage

When people receive a CP14 notice, they generally consider several paths forward. Many choose to pay the balance in full if it’s affordable, which stops all penalties and interest from accruing further. Others explore setting up an installment agreement with the IRS, which allows them to pay the debt over time in monthly payments – the IRS offers both short-term payment plans (120 days or less) and long-term agreements. Some taxpayers review the notice carefully against their own tax records to ensure the amount is correct, particularly if they believe they paid the amount due or if they notice discrepancies in how the IRS calculated the balance.

In situations where the financial hardship is severe, people sometimes research whether they qualify for Currently Not Collectible status or an Offer in Compromise, though these options typically require demonstrating significant financial difficulty. A smaller number of recipients choose to wait, either because they’re expecting a refund from another tax year or because they’re gathering information before deciding how to proceed.

When People Usually Seek Professional Help

Many taxpayers handle CP14 notices on their own, especially when the balance is small and straightforward. However, people often seek assistance from tax professionals, enrolled agents, or tax attorneys in certain situations. Large balances that seem unaffordable often prompt people to consult with someone who can explain all available payment options and negotiate on their behalf. When multiple tax years are involved or when someone has received several IRS notices without understanding the full scope of what they owe, professional guidance can help create a comprehensive resolution strategy.

If the amount on the notice doesn’t match the taxpayer’s records or if there are questions about whether the tax was calculated correctly, professionals can help dispute the amount or request an audit reconsideration. People who are self-employed or have complex tax situations sometimes prefer having representation, particularly if they anticipate ongoing compliance issues. As the collection process escalates toward CP504 or beyond, more people seek professional help because the stakes become higher and the options more complex.

Key Takeaways

- CP14 is the IRS's first formal notice that you have an unpaid tax balance from a filed return

- You're asked to pay within 21 days, though payment plan options exist if you cannot pay in full

- Ignoring this notice leads to additional notices, continued penalties and interest, and eventual enforcement actions

- This is the earliest stage of IRS collections - you have the most options and time to resolve the matter now

- Responding promptly, whether by paying, setting up payments, or contacting the IRS, prevents escalation to more serious notices

This page provides general informational content only and is not affiliated with the IRS or any government agency.