IRS Notice CP504 Explained: What It Means and What Happens Next

By IRS Notices Explained Editorial Team | Reviewed for legal context by David McNickel

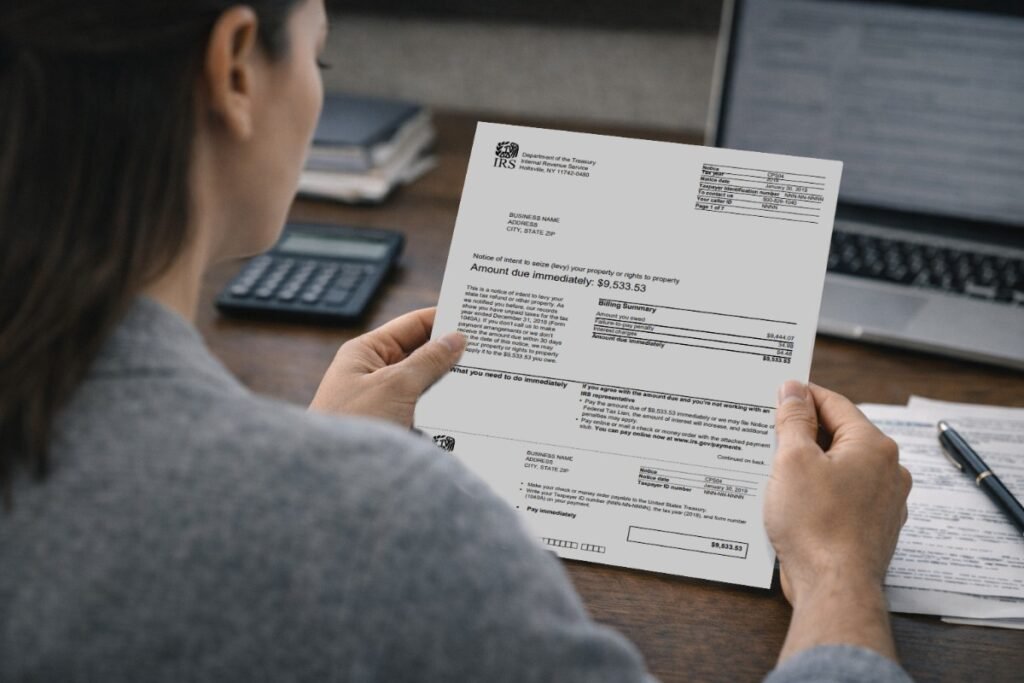

Receiving IRS Notice CP504 means you’ve reached the final stage of the IRS collection notice sequence. This is formally titled “Notice of Intent to Seize Your Property or Rights to Property” or may reference intent to levy.

Unlike the previous notices (CP14, CP501, and CP503), CP504 isn’t just a reminder – it’s the IRS’s legal notification that they intend to enforce collection through liens on your property or levies on your income and bank accounts.

This notice triggers a 30-day window during which you can take action before the IRS proceeds with enforcement. While the situation is serious, you still have rights and options at this stage. Understanding what CP504 means and what you can do about it is essential for protecting your assets and finding a resolution.

IRS Notice Deadline Estimator

Estimate the typical action deadline for selected IRS notice types. For informational purposes only.

Estimate Your Timing Window

Select a notice type and enter the date shown on the notice to view the estimated action deadline and related information.

This estimate is based on typical IRS timing patterns for these notice types, includes weekends in the count, and moves deadlines landing on Saturday or Sunday to the next Monday.

What IRS Notice CP504 Is

IRS Notice CP504 is the final notice before the IRS begins enforced collection actions. It’s sent after you haven’t responded to or paid the balance due shown on CP14, CP501, and CP503. The notice states the IRS’s intent to levy – meaning seize – your property, wages, bank accounts, Social Security benefits, or other assets to satisfy the tax debt.

It also indicates the IRS may file a Notice of Federal Tax Lien, which is a public claim against your property. CP504 includes your current balance with all accumulated penalties and interest, along with a deadline – typically 30 days from the notice date – for you to pay the balance or contact the IRS.

This notice is both a warning and a legal requirement: federal law mandates the IRS must provide this final notice and give you 30 days before beginning levy actions. It represents your last opportunity to resolve the debt voluntarily before the IRS asserts its collection powers.

Why You Received This Notice

You received CP504 because:

- You didn’t pay the balance or establish a payment arrangement after receiving CP14, CP501, and CP503.

- You set up a payment plan previously but defaulted on the agreement, triggering the IRS to accelerate collection efforts.

- You made partial payments but they were insufficient and you didn’t communicate with the IRS about the remaining balance.

- You’ve been unresponsive to all previous IRS attempts to collect the debt over several months.

- Your account has been in collections long enough that the IRS has exhausted the reminder notice process.

- You may have had previous contact with the IRS but failed to follow through on promised actions.

The balance shown on CP504 will be substantially higher than the original amount due on CP14, reflecting months of penalty and interest accumulation.

What the IRS Is Asking You to Do

CP504 demands immediate payment of the full balance within 30 days. If you cannot pay in full, the notice instructs you to call the IRS immediately at the phone number provided to discuss payment options. The notice explains that if you don’t pay or make arrangements within the 30-day period, the IRS will proceed with levy actions, which can include garnishing your wages, seizing funds from your bank accounts, or taking other property. Unlike earlier notices, CP504 is explicit about consequences—it’s not asking you to pay, it’s telling you that failure to pay will result in specific enforcement actions.

The notice also informs you of your right to a Collection Due Process (CDP) hearing if you disagree with the levy or believe the IRS made an error. You must request this hearing within 30 days of the CP504 date to preserve your rights.

What Happens If You Ignore This Notice

Ignoring CP504 leads directly to enforcement actions. Once the 30-day period expires, the IRS can issue a levy without further notice. A levy on wages means your employer will be required to withhold a significant portion of your paycheck and send it to the IRS—often leaving you with only a small allowance for basic living expenses.

A bank levy freezes your account and allows the IRS to seize the funds after a 21-day holding period. The IRS can also levy other income sources like Social Security benefits, retirement distributions, or payments owed to you by clients or customers. Additionally, the IRS may file a Notice of Federal Tax Lien, which becomes a public record attached to all your current and future property.

This lien appears on your credit report, making it difficult to sell property, obtain loans, or conduct financial transactions. Once a levy is in place, reversing it requires proving significant financial hardship or satisfying the debt, which is much more difficult and stressful than resolving the matter before enforcement begins.

How This Notice Fits Into the IRS Collection Timeline

CP504 is the final notice in the standard collection sequence that began with CP14. At this point, you’ve received four notices over approximately 4-6 months, each giving you the opportunity to address the debt. CP504 marks the transition from voluntary compliance to enforced collection.

After CP504, there are no additional reminder notices and the next step is action by the IRS. If you ignore CP504 and the 30-day period expires, the IRS will typically issue a levy within weeks or months, depending on their collection priorities and your specific situation. The Notice of Federal Tax Lien may be filed before, during, or after CP504, depending on the balance size and IRS internal procedures.

Once enforcement actions begin, resolving the situation becomes more complicated because you’re now dealing not just with the debt, but with active liens and levies that affect your day-to-day finances. CP504 represents the last clear opportunity to negotiate and resolve the debt before the IRS takes control of the process.

Common Questions About The IRS CP504 Notice

Is this the absolute last notice before enforcement?

Yes, CP504 is the final notice. The IRS is legally required to send it at least 30 days before levying your assets.

Can I still set up a payment plan after receiving CP504?

Yes, you can still establish an installment agreement, but you must act immediately within the 30-day window. Once a levy is issued, options become more limited.

What is a Collection Due Process hearing?

It’s a hearing with the IRS Office of Appeals where you can contest the levy or lien, propose collection alternatives, or raise legal defenses. You must request it within 30 days.

Will the IRS definitely levy my accounts if I don't respond?

While not automatic, it’s highly likely. The IRS has issued CP504 with the intention of enforcing collection if you don’t pay or make arrangements.

How much will the IRS take from my paycheck?

The amount depends on your filing status and dependents, but wage levies often leave you with minimal income—sometimes just enough for basic living expenses.

Can I get the penalties removed at this stage?

Penalty abatement is possible if you qualify, but time is limited. You’ll need to address this while also resolving the immediate levy threat.

What if I can't afford any payment?

Contact the IRS to discuss Currently Not Collectible status or submit financial information showing genuine hardship. Professional help is advisable at this stage.

What Options People Typically Consider at This Stage

When people receive CP504, they recognize the urgency and act quickly. Many pay the balance in full if at all possible, even if it means using savings, borrowing from family, or taking a loan – because the alternative of wage garnishment or account seizure is more financially damaging.

Others immediately contact the IRS to set up an installment agreement, understanding that even a payment plan they can barely afford is better than having their wages levied. Some people request a Collection Due Process hearing, particularly if they believe the amount is incorrect, if they have grounds to dispute the debt, or if they need time to explore resolution options while preventing immediate enforcement.

Those facing severe financial hardship gather documentation to prove their situation and request Currently Not Collectible status or prepare an Offer in Compromise application. Many people at this stage realize they need professional representation and hire an enrolled agent, CPA, or tax attorney to negotiate on their behalf and protect their rights. Very few people ignore CP504—those who do typically face immediate and severe financial consequences.

When People Usually Seek Professional Help

CP504 is the stage where professional representation becomes most common and most valuable. The complexity of dealing with imminent levies, understanding Collection Due Process rights, and negotiating with IRS revenue officers makes professional help nearly essential for many taxpayers. Large balances exceeding $25,000 almost always warrant professional representation because the stakes are high and the resolution options are complex. People who’ve never dealt with IRS collections before often feel overwhelmed by CP504 and seek professionals who can navigate the process and communicate with the IRS on their behalf.

When someone has multiple tax years in collections, unfiled returns, or complicated financial situations, professionals can develop a comprehensive strategy that addresses all issues simultaneously. Those who need to request a CDP hearing typically hire representation because these hearings involve legal arguments and procedural requirements that are difficult to manage alone. Self-employed individuals and business owners facing CP504 particularly benefit from professional help because levies can affect business accounts and operations.

At this stage, the cost of professional help is often offset by the value of preventing levies, reducing penalties, and achieving more favorable payment terms.

Key Takeaways

- CP504 is the final notice before the IRS begins enforcing collection through levies and liens

- You have 30 days from the notice date to pay the balance, set up payment arrangements, or request a Collection Due Process hearing

- Ignoring this notice results in wage garnishment, bank account seizure, and/or a federal tax lien

- Payment plan options still exist, but you must act immediately to prevent enforcement

- Professional representation is strongly advisable at this stage given the complexity and severity of potential consequences

This page provides general informational content only and is not affiliated with the IRS or any government agency.