IRS Notice LT11 / CP90 Explained: What It Means and What Happens Next

By IRS Notices Explained Editorial Team | Reviewed for legal context by David McNickel

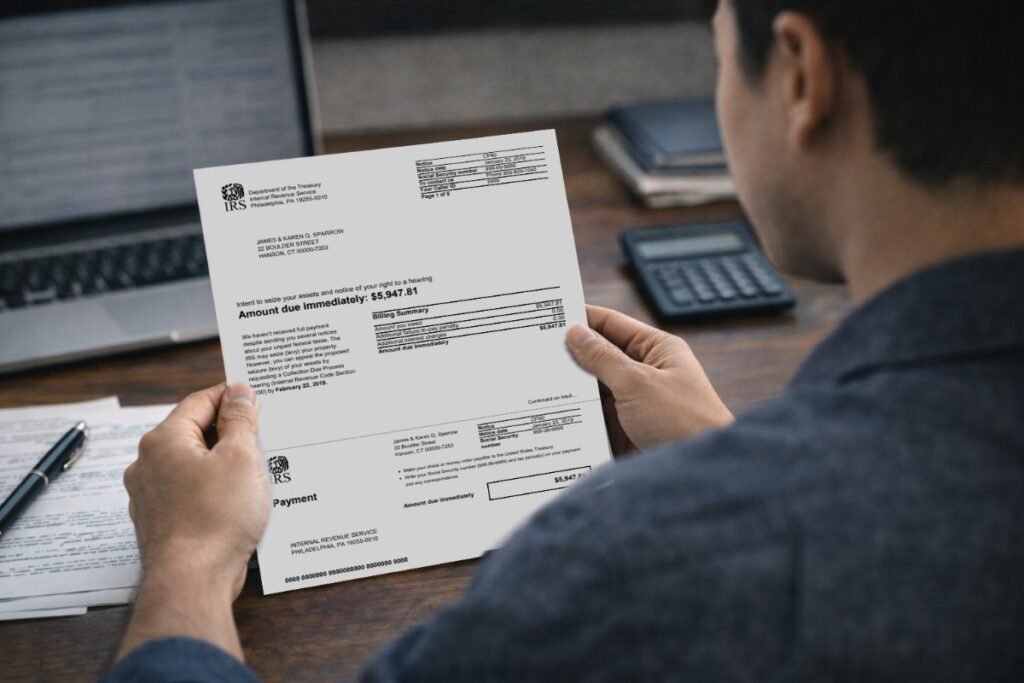

If you’ve received IRS Notice LT11 or CP90, you’re facing one of the most serious notices the IRS sends. This is the “Final Notice of Intent to Levy and Notice of Your Right to a Hearing,” and it means the IRS is preparing to seize your assets – including wages, bank accounts, Social Security benefits, or property – to satisfy an unpaid tax debt.

Unlike earlier collection notices, LT11/CP90 represents the IRS’s formal legal notification required before they can proceed with enforcement. This notice triggers specific rights and deadlines that you must understand and act upon. While the situation is urgent, you still have options and legal protections.

This notice demands immediate attention, but understanding what it means and what happens next can help you navigate this critical stage. The LT11/C90 is one of many IRS notices – you can review all notice types in our IRS Notices guide.

IRS Notice Deadline Estimator

Estimate the typical action deadline for selected IRS notice types. For informational purposes only.

Estimate Your Timing Window

Select a notice type and enter the date shown on the notice to view the estimated action deadline and related information.

This estimate is based on typical IRS timing patterns for these notice types, includes weekends in the count, and moves deadlines landing on Saturday or Sunday to the next Monday.

What IRS Notice LT11 / CP90 Is

IRS Notice LT11 and Notice CP90 are essentially the same notice with different designations – both are the “Final Notice of Intent to Levy and Notice of Your Right to a Hearing.” The IRS sends this notice when they intend to levy your property or rights to property to collect an unpaid tax debt.

It’s sent either after you’ve gone through the standard collection notice sequence (CP14, CP501, CP503, CP504) without resolution, or in cases where the IRS has accelerated collection efforts. This notice informs you that the IRS will levy unless you pay the amount in full, make payment arrangements, or request a Collection Due Process (CDP) hearing within 30 days.

The levy authority granted by this notice allows the IRS to garnish wages, seize bank accounts, intercept Social Security benefits, place liens on property, and take other collection actions. This is a legally required notice – the IRS cannot proceed with most levy actions without first providing LT11/CP90 and giving you 30 days to respond.

Why You Received This Notice

You received LT11 or CP90 for one of these reasons:

- You have an unpaid tax balance that has gone through the entire collection notice process without payment or resolution.

- You previously had a payment arrangement (installment agreement) that defaulted, and the IRS has accelerated collection.

- The IRS has determined your account warrants immediate collection attention, possibly due to the balance size or collection potential.

- You have multiple years of unpaid taxes and the IRS has consolidated collection efforts.

- You may have had contact with an IRS revenue officer who is actively working your case.

- Your account has been transferred to an Automated Collection System (ACS) unit that is pursuing aggressive collection.

- The IRS has concerns about your ability to pay in the future and wants to secure collection now.

Unlike earlier notices which are automatically generated, LT11/CP90 often indicates more direct IRS involvement in your case.

What the IRS Is Asking You to Do

LT11/CP90 demands one of three actions within 30 days:

- Pay the full amount due,

- Contact the IRS immediately to make payment arrangements,

- Request a Collection Due Process (CDP) hearing.

The notice explicitly states that if you don’t take one of these actions, the IRS will proceed with levy actions. If you request a CDP hearing within the 30-day window, the IRS generally must pause collection enforcement while the hearing process is ongoing – this is a critical protection.

The notice provides instructions for requesting a CDP hearing using Form 12153 and explains your right to bring relevant issues before the IRS Office of Appeals. Unlike earlier notices that simply requested payment, LT11/CP90 is the IRS’s formal legal notification of intent to levy, which activates specific taxpayer rights under federal law.

The 30-day response deadline is strict – missing it means losing your right to a CDP hearing and allowing the IRS to proceed with enforcement without further notice.

What Happens If You Ignore This Notice

Ignoring LT11/CP90 has immediate and severe consequences. Once the 30-day period expires without response, the IRS can issue levies without any additional notice to you. A wage levy (or wage garnishment) will be sent to your employer, requiring them to withhold a substantial portion of your paycheck – often leaving you with only a small exempt amount based on filing status and dependents.

A bank levy will freeze your accounts and allow the IRS to seize the funds after a 21-day holding period. The IRS can also levy Social Security benefits, retirement account distributions, rental income, accounts receivable, and virtually any other income or payment owed to you. Additionally, the IRS may file a Notice of Federal Tax Lien, which becomes a public record and severely impacts your credit and ability to conduct financial transactions.

Continuous levies can remain in effect indefinitely, meaning every paycheck or payment you receive is automatically sent to the IRS until the debt is satisfied. By ignoring this notice, you forfeit your right to a Collection Due Process hearing, eliminating one of your most important legal protections.

How This Notice Fits Into the IRS Collection Timeline

LT11/CP90 represents the enforcement phase of IRS collections. For most taxpayers, this notice comes after months or years of prior notices – typically after CP14, CP501, CP503, and CP504 have been sent without resolution. However, in some cases, the IRS may skip the standard sequence and send LT11/CP90 earlier if they determine immediate collection action is warranted.

This can happen when there’s a large balance, when the IRS believes you’re transferring assets, when a revenue officer is assigned to your case, or when a previous payment agreement has failed. After LT11/CP90, there are no further notices – the next step is the levy itself. The timeline from this notice to actual enforcement depends on whether you respond: if you request a CDP hearing, enforcement is typically suspended during the appeals process, which can take months.

If you don’t respond, levies can be issued immediately after the 30-day period ends. Some taxpayers receive LT11/CP90 multiple times for different tax years or if their situation changes, but each notice triggers a new 30-day response window.

Common Questions About The IRS CP504 Notice

Is this the same as CP504?

They’re similar but LT11/CP90 is more serious. It specifically grants you Collection Due Process hearing rights and often indicates more aggressive IRS collection efforts.

What is a Collection Due Process hearing and should I request one?

It’s an independent hearing with the IRS Office of Appeals where you can contest the levy, propose alternatives, or raise collection issues. Requesting it within 30 days suspends enforcement.

What is a Collection Due Process hearing?

It’s a hearing with the IRS Office of Appeals where you can contest the levy or lien, propose collection alternatives, or raise legal defenses. You must request it within 30 days.

Can I still set up a payment plan after receiving this notice?

Yes, but you must contact the IRS immediately. Once a levy is issued, it’s much harder to negotiate favorable terms.

How much will the IRS take from my paycheck?

Wage levies leave you with a minimal exempt amount based on standard deduction and dependents—often just a few hundred dollars per pay period regardless of your actual expenses.

Can they take my Social Security or retirement income?

Yes, the IRS can levy up to 15% of Social Security benefits and can levy retirement account distributions, though some protections exist for certain retirement accounts not yet distributed.

What if I can't afford any payment?

You may qualify for Currently Not Collectible status or an Offer in Compromise, but you must provide detailed financial information and typically need professional help to navigate these options.

What Options People Typically Consider at This Stage

When people receive LT11/CP90, they immediately recognize the gravity of the situation and take decisive action. Many who have the resources pay the balance in full to stop the collection process entirely. Others immediately contact the IRS or a tax professional to set up an installment agreement, understanding that even a payment plan with terms they find difficult is preferable to having wages garnished or accounts seized.

A significant number request a Collection Due Process hearing, especially when represented by a professional, because this pauses enforcement and provides time to explore all options. Some people use the CDP hearing process strategically to propose an Offer in Compromise or to argue for penalty abatement or other relief. Those facing genuine financial hardship gather extensive financial documentation to prove Currently Not Collectible status or to support reduced payment arrangements. Many taxpayers at this stage accept that professional representation is necessary and hire an enrolled agent or tax attorney to handle negotiations and protect their rights.

Very few people ignore LT11/CP90 once they understand what it means—those who do typically suffer immediate financial harm.

When People Usually Seek Professional Help

LT11/CP90 is where professional representation becomes not just advisable but often essential. The complexity of Collection Due Process rights, the need to prepare for an appeals hearing, and the high stakes of imminent levies make professional help extremely valuable. Tax attorneys, enrolled agents, and CPAs who specialize in IRS collections understand how to navigate the CDP process, what arguments appeals officers respond to, and how to structure proposals that the IRS is likely to accept.

People with balances over $50,000 almost universally seek representation at this stage because the financial and legal consequences are severe. Those who need to propose an Offer in Compromise or request Currently Not Collectible status require professional help because these applications demand detailed financial disclosure and specific legal arguments.

Business owners facing LT11/CP90 particularly need professionals because levies can affect business bank accounts and disrupt operations. When revenue officers are involved—which is common at the LT11/CP90 stage—having a professional who understands how to work with revenue officers and negotiate effectively is crucial. The cost of representation is often recovered through better negotiated terms, penalty abatement, and preventing the financial damage that levies cause.

Key Takeaways

- LT11/CP90 is the final notice before the IRS levies your wages, bank accounts, and other property

- You have 30 days to pay in full, set up payment arrangements, or request a Collection Due Process hearing

- Requesting a CDP hearing within 30 days suspends enforcement and gives you time to explore options

- Ignoring this notice results in immediate wage garnishment, account seizure, and loss of legal protections

- Professional representation is strongly advisable given the complexity of CDP rights and the severity of enforcement actions

This page provides general informational content only and is not affiliated with the IRS or any government agency.